Published on April 28, 2026

Susan manages a 30 million dollar family office. Last year, her bond allocation generated exactly 2.1% returns while stocks soared 18%. She is frustrated. She watches corporate bond yields and sees 4-5% available on investment-grade bonds. She reads about sophisticated investors earning higher returns from something called private credit. She asks her advisor: ‘What am I missing? Why can I not access these higher yields?’

The answer is complex. Private credit does often offer higher yields than traditional bonds, but it comes with real trade-offs that marketing materials frequently downplay: illiquidity, opacity, and economic risk. This guide explains what private credit actually is, why returns can be higher, what risks you genuinely face, what ‘accessing’ private credit really means in practice, and how it fits within the broader private market ecosystem. Unlike promotional material that emphasizes yield and downplays risk, we examine both opportunity and substantial limitations. We also address the most commonly repeated claims about the asset class and explain where they oversimplify or mislead.

What is Private Credit? Definition and Reality

Private credit refers to loans made by non-bank lenders (typically large private credit funds) directly to companies, negotiated between lender and borrower rather than traded on public markets. Unlike publicly traded bonds, which change hands continuously and have transparent market prices updated daily, private credit loans are held to maturity by the originating fund and priced infrequently, often only quarterly. The asset class has grown explosively from a niche strategy to a multi-trillion-dollar industry, attracting pension funds, insurance companies, family offices, and increasingly retail investors seeking higher income than traditional bonds provide.

However, the mechanics are often misunderstood or deliberately obscured in marketing materials. When you invest in private credit, you typically do not own individual loans directly. Instead, you own a stake in a private credit fund, much like owning shares in a mutual fund. The fund originates loans, holds them until maturity, monitors borrowers, enforces covenants, and distributes cash to investors according to its stated terms and fee structure. This matters profoundly because it affects liquidity, timing of cash flows, the actual return you receive after all costs, your ability to control investment decisions, and your legal standing if the fund faces difficulty.

When a borrower makes an interest payment on a loan, that money goes first to the fund, not directly to you. The fund then deducts management fees (typically 1-2% annually), performance fees (sometimes 20% of annual profits), administrative costs, and reserves before distributing what remains to investors. If the borrower prepays, restructures, defaults, or the loan is sold, the timing and amount of your return changes. This is fundamentally different from owning a public bond directly, where you receive interest payments independently and can sell your position at will through public markets.

The terms ‘private credit,’ ‘private debt,’ ‘direct lending,’ and ‘non-bank lending’ are used interchangeably throughout the industry. What they have in common: loans arranged directly between non-bank lenders and borrowers outside traditional bank channels, held to maturity, and priced infrequently outside public markets.

Why Yields Are Higher: Understanding the Return Premium

Investment-grade public bonds currently yield 3-5%. Private credit loans commonly offer 8-12% gross coupons. This substantial yield premium is not free money or evidence of inefficiency. It exists because investors are compensating for specific risks that are often downplayed in promotional materials: illiquidity, credit risk, valuation opacity, limited regulatory oversight, and limited recourse if loans default or alternative investment funds face stress.

Private credit borrowers are typically mid-market companies that cannot access traditional bank financing or public bond markets. They may be smaller, more leveraged, faster-growing, in transition, or have other characteristics that make banks reluctant to lend. Unlike large corporations with investment-grade debt traded on public markets, these borrowers face meaningfully higher risk of business failure, especially when economic conditions deteriorate, credit tightens, or consumer demand drops. Default risk is real, material, and increases substantially in downturns. Higher yields are the price investors pay for accepting this credit risk, not proof that the investment is intrinsically safe or ‘better’ than public bonds.

Additionally, the yield premium compensates investors for illiquidity. You cannot sell your position in a private credit fund mid-term the way you can sell public bonds. If you absolutely must raise capital, you may be able to sell on the secondary market, but only at discounts of 10-25% or more depending on market conditions and fund stress. You are locked in for 5-10 years or longer. Investors historically demand substantial yield premiums for surrendering liquidity, and private credit represents one of the most illiquid investments available to individual investors. That premium is very real and deserves serious scrutiny: Is the additional yield worth being unable to access your capital for a decade?

The critical question is not whether yields are higher – they clearly and obviously are – but whether the additional yield fairly compensates for the added risks and constraints you are accepting. Current academic and industry research suggests the answer may be only marginally positive at best, and in some strategies and time periods, quite uncertain or negative.

What You Actually Earn: From Gross Coupon to Net Return

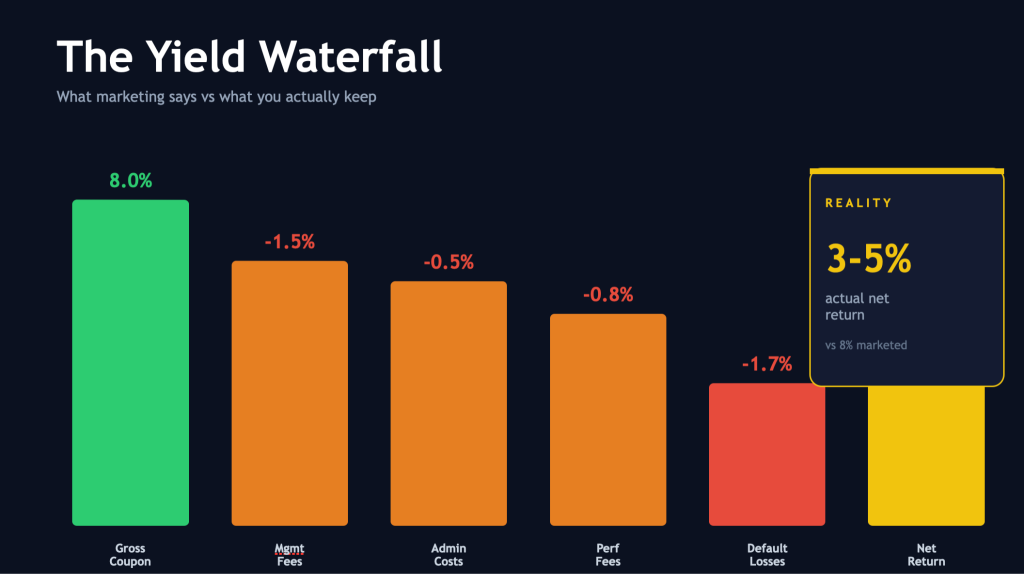

A fund marketing an ‘8% coupon’ or promising ‘8% returns’ does not mean you earn 8% annually. Your actual net return is substantially and materially lower. This is the critical arithmetic that marketing materials routinely omit, obscure, or present in misleading ways.

Consider a realistic but not extreme example: A portfolio of loans yields 8% gross coupon. However, after the fund’s 1.5% management fee (charged annually on invested capital), 0.5% in administrative costs, and a 20% performance fee on profits (equivalent to roughly 0.8% annually in this scenario), you are down to approximately 5.2% net of fees, before accounting for any defaults or losses. If the portfolio experiences a typical 2-3% annual default rate (a reasonable and conservative assumption based on varying fund performance across cycles), and 33% recovery on defaults (per Federal Reserve research, significantly lower than the inflated 75% sometimes claimed in marketing), expected loss is another 1.3-2%, bringing your net return to roughly 3.2-4%. This is technically still above investment-grade bonds yielding 3-4%, but the margin is extremely narrow and assumes everything goes according to plan with no additional stress, redemption pressure, or portfolio restructuring.

This arithmetic is systematically hidden or downplayed in marketing materials and pitch books, which emphasize gross coupon and gross returns rather than net-of-fee returns. It is also highly dependent on actual default experience, which varies dramatically across different economic cycles, strategies, manager quality, and market conditions. During downturns and stress periods, losses accelerate, recoveries decline sharply, and redemption pressure can force funds to sell assets at severe discounts, further reducing returns to existing investors.

The essential takeaway: private credit may offer 5-7% net returns in stable economic conditions, providing modest enhancement over investment-grade bonds or perhaps equivalent to well-chosen high-yield bond funds, but not the 8-12% that marketing materials highlight. This distinction matters substantially for long-term wealth accumulation.

Valuation Opacity and Regulatory Concerns

Financial regulators, including the Federal Reserve, SEC, and international regulators, have explicitly raised concerns about private credit valuation practices and the opacity of the entire asset class. The issue is fundamental and structural: unlike public bonds, which have transparent, market-determined prices updated continuously throughout trading days, private credit funds price portfolios infrequently – often only quarterly or sometimes even less often. This means losses, stress, and deteriorating credit quality can accumulate for months before investors see their holdings marked down in quarterly statements.

In 2024 and early 2025, multiple large private credit funds disclosed significant markdowns ranging from 5-15% and suspended investor redemptions entirely, revealing that valuations had substantially lagged behind underlying economic stress in borrower portfolios. Investors who thought they were earning steady, stable returns discovered large losses had accumulated unrecognized in their statements. The smooth, stable returns that private credit marketing emphasizes can substantially reflect delayed loss recognition rather than genuine economic insulation from risk. When valuations eventually reset to reflect reality, investors discover losses they could not see or price in on prior statements.

Additionally, private credit funds face significantly less regulatory oversight and disclosure requirements than banks, insurance companies, or public bond funds. Information disclosure to investors is often limited and lagging. Fund managers have substantial discretion over valuation methodologies, reserve policies, distribution timing, and loss recognition timing. Investors typically lack detailed visibility into individual loan performance, collateral quality, covenant compliance status, or problem loans until significant stress surfaces or quarterly reports are issued.

This structural opacity creates a critical and material behavioral and financial risk: by the time you see losses in your quarterly statements, it may be too late to rebalance, reduce exposure, or transfer positions. You are locked in with an illiquid fund experiencing stress, unable to protect yourself, unable to realize prices, and unable to exit except at severe discounts.

Default Rates and Recovery: The Hard Data

Claims that private credit default rates are ‘typically 1-3% annually’ are presented with more confidence than warranted, given actual variability in experience. Direct lending funds focused on stable mid-market companies may average low single-digit default rates during economic expansions, but rates vary enormously by fund manager, strategy, borrower profile, leverage, and position in the credit cycle. Some strategies (direct lending to stable profitable companies) show lower defaults; others (mezzanine lending, distressed, leveraged) show meaningfully higher rates.

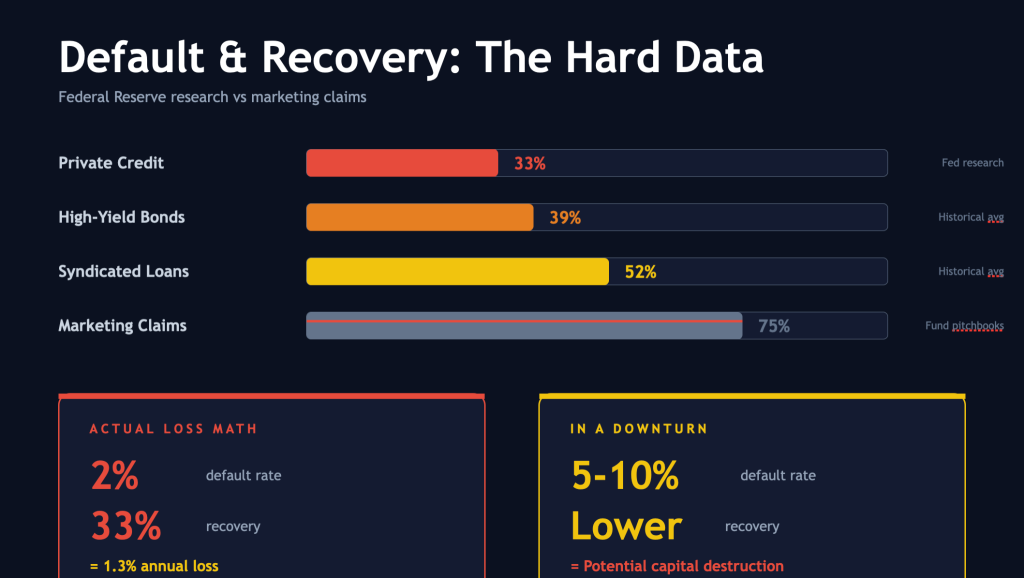

More importantly, recovery rates for private credit loans are significantly and substantially lower than suggested by promotional material. Federal Reserve research, specifically cited by the SEC, indicates post-default recovery values around 33 percent for private credit loans. Compare this to 52 percent for syndicated bank loans and 39 percent for high-yield bonds. This means that when a private credit loan defaults, investors recover roughly one-third of principal on average. The other two-thirds represents a permanent loss. This is a crucial fact that fundamentally affects return calculations and portfolio risk.

These recovery rates have serious implications for actual performance. A 2% annual default rate with 33% recovery represents a 1.3% annual loss in principal value, not a minor event. Combined with coupon income, management fees, administrative costs, and other friction costs, this substantially reduces net returns compared to marketing expectations. And 2% default is not extreme during normal economic times – during recessions, credit tightening, or stress periods, default rates can rise to 5-10% or higher, which would be catastrophic to a portfolio’s performance and to investor returns.

The modern private credit market at its current multi-trillion-dollar scale and complexity has not yet experienced a major downturn or stress event. This is crucial context often omitted. Claims about ‘2008 private credit default rates’ should be disregarded entirely – the market in 2008 was far smaller, differently structured, less leveraged, and not directly comparable to the current environment.

Liquidity, Illiquidity, and Practical Constraints

Private credit funds typically lock capital for 5-10 years by contractual terms. You cannot redeem your investment on a whim or when circumstances change. If you absolutely must access capital, you may be able to sell your stake on the secondary market for private credit funds, but only at significant discounts of 10-25% or more, depending on market conditions, fund performance, and overall market stress. This illiquidity is not a minor inconvenience or a technical detail in fund documents. It is a fundamental and binding structural feature with material financial implications.

Before committing capital to private credit, ensure you have substantial liquid reserves specifically for emergencies (12-24 months of living expenses in cash and liquid, safe investments) and that you genuinely will not need the allocated capital during the lock-up period. If your business needs capital, a family emergency occurs, investment priorities shift, or your personal financial situation changes, you cannot simply exit without taking a significant loss. This constraint is binding and real and deserves the most serious consideration.

Additionally, during stress periods, market downturns, and credit market dislocations, secondary market liquidity for private credit fund stakes evaporates entirely. Recent episodes have clearly shown that when multiple funds need to return capital simultaneously, they face severe markdown pressure and implement redemption restrictions, trapping investors mid-crisis with no ability to exit except at severe losses.

Illiquidity is the structural cost of accessing higher yields in private credit. It is not negotiable, it is binding, and it deserves the highest-level consideration in your allocation decision.

Banks, Private Credit, and the Financial System

A common narrative holds that ‘banks have largely withdrawn from mid-market lending, creating a gap that private credit fills.’ This is only partially true and risks oversimplifying the market structure. Post-2008 regulation did reduce banks’ appetite for certain types of lending and increased their regulatory capital requirements. This did create opportunities for non-bank lenders. However, banks remain deeply and actively involved in corporate lending and are increasingly providing financing facilities, backup credit lines, collateral financing, and other support roles within private credit transactions themselves. The relationship between banks and private credit is not one of simple replacement but rather symbiotic and deeply interconnected.

Moreover, banks themselves are significant investors in private credit funds through their proprietary trading divisions, pension plans, and insurance subsidiaries. Large commercial and investment banks have also established their own private credit platforms. If stress hits the private credit market, it directly impacts bank balance sheets, creating feedback loops and systemic risks that regulators monitor closely.

The point: private credit is not independent from the broader financial system. Economic stress that hurts borrowers also hurts private credit investors and the banks financing or investing in private credit, creating correlated losses and potential systemic feedback loops.

How to Allocate and Conduct Due Diligence

If you allocate to private credit after careful consideration of these risks: Diversify broadly across 4-6 different funds with different strategies and managers. Request 10-year audited performance histories and verify independently. Demand complete fee transparency. Calculate net-of-fee returns, not gross coupons. Limit allocation to 10-15% of fixed income maximum. Maintain substantial liquid reserves. And remain deeply skeptical of any narrative claiming private credit is ‘safe,’ ‘stable,’ or immune to downturns.

Private credit has a legitimate role in portfolios, but only when appropriately sized, carefully selected, and honestly evaluated. The promotional narrative is often misleading. Approach with realistic expectations and proper due diligence.

Conclusion: The Honest Assessment

Susan’s 2.1% bond return was suboptimal and reflected either poor bond allocation or overly defensive positioning. Better bond allocation or a modest high-yield allocation would have improved results. Private credit might contribute as well, but not by the margin marketing suggests.

A realistic private credit allocation might contribute 5-7% to overall portfolio income, marginally above traditional bonds but with considerably higher illiquidity, opacity, complexity, and default risk. Whether this trade-off is worthwhile depends entirely on your specific situation, time horizon, risk tolerance, and genuine comfort with being locked into illiquid investments for a decade.

Private credit has a legitimate, meaningful role in diversified portfolio construction for appropriate investors, but only when appropriately sized, carefully selected, backed by serious due diligence, and honestly evaluated. The promotional narrative that frames it as ‘bonds with extra yield and no downside’ is fundamentally misleading. Real private credit involves real risks that surface with a lag, operate within opacity that regulators have questioned, and depend on recovery rates far below what promotional materials imply.

If you allocate, do so eyes wide open: expect 5-7% net returns not 8-12%, maintain substantial liquid reserves, demand fee transparency, diversify broadly, and plan for the possibility that downturns affect private credit as much as any other form of debt investment.