Published on April 10, 2026

Why Investors Are Asking About Alternative Investment Funds

Why do institutional investors and wealthy families consistently outperform ordinary investors? Why do pension funds earn 12-15% returns while individual investors struggle to achieve 7-8%? The answer lies in something most retail investors never seriously consider: alternative investment funds.

Unlike the mutual funds and ETFs you can buy at any brokerage, Alternative Investment Funds represent an entirely different approach to investing – one that has historically been locked away from ordinary investors due to regulatory restrictions and high minimums. But investors increasingly realize they are missing significant wealth-building opportunities.

They ask fundamental questions: What returns will I actually make after fees? Will I be able to access my money if circumstances change? Can I truly evaluate the manager’s quality? How much of my portfolio should be in alternatives? And does this actually make sense for my situation? This guide answers these questions directly, based on what real investors want to know about alternative investment funds.

For decades, alternative investment funds were exclusively available to billionaires, large pension funds, university endowments, and major institutions. The exclusivity was intentional and deliberate. Fund managers didn’t want to deal with retail investors’ questions, complaints, and demands for constant communication.

They preferred institutional clients who understood illiquidity and took a hands-off approach. But technology and regulatory changes are fundamentally transforming that landscape. Understanding what is an alternative investment fund is now becoming essential for any serious investor seeking to optimize long-term wealth and move beyond the limitations of public market returns alone.

We will address the specific concerns investors actually have: realistic return expectations versus hype, how fees impact your actual take-home gains, liquidity constraints and what they mean for your planning, assessing manager quality when you lack industry connections, tax consequences on your net returns, diversification strategy and allocation percentages, practical steps to get started, and honest tradeoffs you must understand before committing capital.

By the end, you will have a clear framework for determining whether AIF investment (and an alternative investment marketplace like Gamma Prime) makes sense in your specific financial situation.

What Are Alternative Investment Funds? Understanding the Basics

Let’s start with the fundamental definition: what is an alternative investment fund? An alternative investment fund is a pooled investment vehicle that invests in non-traditional assets or employs non-traditional strategies – things you cannot simply walk into a brokerage and buy like Apple stock. Instead of traditional stocks and bonds, alternative investment funds invest in the private market, real estate properties, infrastructure projects, specialized trading strategies, commodities, or complex derivatives.

When you buy Apple stock on the public market, you own one of millions of shares trading daily with transparent pricing. In an alternative investment fund, you own a legal stake in a private company that the fund manager is actively improving through management changes, operational restructuring, and strategic acquisitions, working to eventually sell that company for significant profit five to ten years later. That fundamental difference – from passive holding to active management, from liquid to illiquid, from transparent public pricing to opaque valuations updated annually – defines the entire alternative investment category.

When people search for what is AIF, they frequently encounter terminology confusion and acronyms. AIF stands for Alternative Investment Fund. You will hear people use AIF alternative investment fund, what is an AIF, and simply alternative investment fund completely interchangeably. They all mean the exact same thing. Some regulatory bodies use AIF as the formal legal classification. Some use alternative investment fund descriptively in their literature.

Both terms are completely correct and describe identical vehicles. Do not allow terminology differences to create confusion. Whether someone calls it an AIF, alternate investment fund, or alternative investment fund, they are describing the same basic structure: a professionally-managed pooled vehicle managing capital deployed into non-traditional investment strategies.

The explosive growth of alternative investment funds over the past two decades directly reflects rising investor demand for different and superior returns. Twenty years ago, alternatives represented tiny specialty investments available only to ultra-wealthy families living in Manhattan or other financial centers. Today, they are thoroughly mainstream across the entire investment industry.

Pension funds allocate 15-25% of portfolios to alternatives. University endowments allocate 30-40% of assets. Family offices allocate 20-40% of capital. This is not speculation or hype. It reflects decades of rigorous data and documented results proving alternatives provide returns that public markets alone cannot reliably deliver. Yale’s endowment, managed by one of the world’s best and most careful investing teams with access to top managers globally, allocates 38% of assets to alternatives. Harvard allocates similar amounts. Stanford allocates aggressively to alternatives.

These extraordinarily sophisticated institutions do not make allocation decisions lightly. Their sustained commitment to alternatives reflects an informed institutional conclusion: these vehicles genuinely generate superior long-term returns justifying the illiquidity, complexity, and fees.

How Alternative Investment Funds Work: The Real Process

Understanding how AIF investment actually operates in practice requires grasping the complete multi-year process. It differs fundamentally from buying mutual funds at a brokerage. When you invest in an alternative investment fund, you commit capital upfront, but the manager does not immediately deploy it. Instead, you commit to providing capital when the manager identifies and evaluates specific opportunities meeting their criteria.

This process is called a capital call. The manager contacts you when they need your capital, you wire funds, and deployment occurs. This structure gives managers certainty about available capital while providing you flexibility during the commitment period. Over subsequent months or years, the manager systematically deploys that committed capital according to the fund’s stated investment strategy and objectives. If it is a private equity fund, the manager is acquiring undervalued companies and improving them. If it is venture capital, the manager is backing promising early-stage startups. If it is real estate, the manager is purchasing properties with enhancement potential.

You are not involved in daily operational decisions. You are paying professional managers with decades of experience to make those critical decisions well.

The timeline and fee structure matter significantly to your actual returns. Most alternative investment funds charge management fees of 1-2% of assets annually regardless of performance or results. This covers operations, salaries for the investment team, infrastructure, and ongoing business expenses.

They additionally charge performance fees, typically 20% of profits the fund generates. So if the fund generates 20% returns, the manager takes 20% of those profits above the target, leaving you 80% of the profits. This fee structure explains precisely why manager selection matters profoundly for your actual results.

A truly excellent manager generating 18% returns after paying 3.6% total fees delivers 14.4% net returns to you – exceptional and life-changing performance. A mediocre manager generating 8% returns still charges identical fees, leaving you 4.4% net returns – significantly worse than a low-cost index fund. Manager quality directly determines your actual take-home returns.

The complete investment lifecycle typically runs 5-10 years from initial commitment through final distribution. You commit capital in year one. Capital gradually deploys over years one through three as managers identify and execute deals. The manager builds value during years three through seven through operational improvements and strategic actions.

Exit events occur in years seven through ten when managers sell companies or take them public. Distributions return capital and accumulated profits to you during this entire period. This is completely different from stock investing, where you can buy and sell shares in seconds at market prices.

The extended timeline is simultaneously a feature and a constraint. It enables managers to make long-term operational improvements that generate exceptional returns unavailable to public companies. But it locks your capital away, preventing access if circumstances change or better opportunities emerge. Understanding this multi-year timeline before committing capital is absolutely critical.

Real Return Expectations: What Investors Actually Make

The critical question every investor asks: What returns will I actually make? This is where realistic expectations matter significantly. What are alternative investment funds really capable of generating over the long term? The answer depends on the specific category and manager quality. Private equity funds targeting mid-market companies historically generate 12-18% annual returns net of fees.

Venture capital funds targeting early-stage companies pursue 20-30% annual returns but with higher failure rates requiring diversification. Real estate funds targeting value-add opportunities generate 8-12% annual returns. Infrastructure funds pursuing stable assets generate 6-8% annual returns. These are returns after all fees deducted. These numbers matter because they are what you actually keep, not gross returns before fees.

Compare this to public market returns for context. The S&P 500 historically returns approximately 10% annually over long periods. So a net 11% from private equity seems only marginally better. But that seemingly small difference compounds dramatically over decades. A 100,000 dollar investment over 20 years at 10% becomes 673,000 dollars. That same investment at 11% becomes 806,000 dollars.

The difference is 133,000 dollars of additional wealth – 20% more from just 1% higher annual returns. That is why sophisticated investors carefully allocate capital to alternatives. The long-term compounding advantage over decades is genuinely substantial. However, achieving these returns requires selecting excellent managers with proven track records. Many alternative funds underperform public markets, particularly in bull markets when stocks soar unexpectedly. Manager selection is not optional. It is the entire game. Bad managers destroy capital despite high fees.

Types of Alternative Investment Funds: Which Strategy For You?

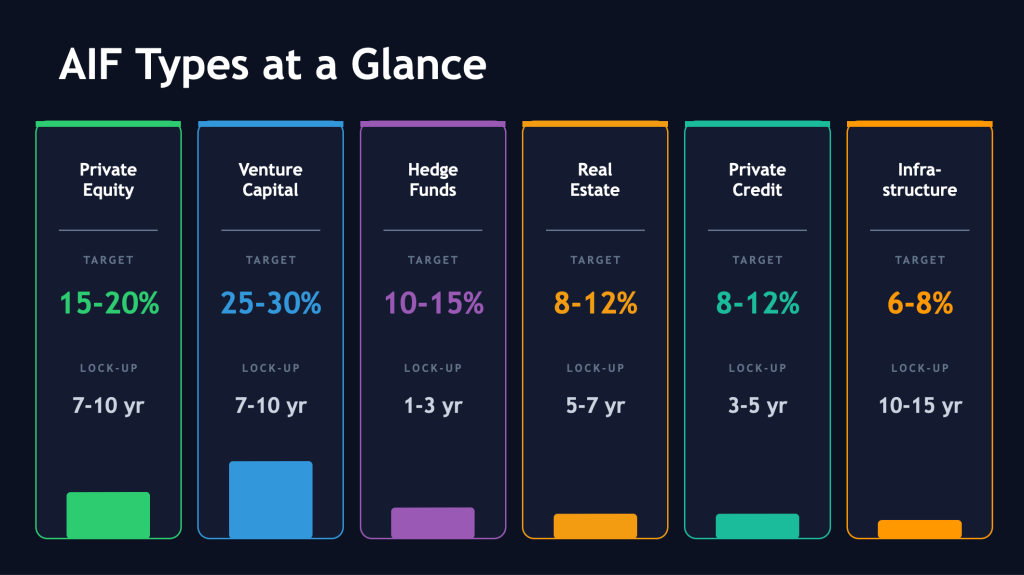

Different alternative investment fund categories pursue fundamentally different investment strategies with different return profiles and risk characteristics. Private equity funds acquire established companies with solid products but outdated management, improve operations through better management and strategic acquisitions, and sell for profit 5-7 years later. They target 15-20% net returns.

Venture capital funds back early-stage companies betting on exponential growth in emerging markets. They target 25-30% net returns but accept that most portfolio companies fail. Hedge funds employ sophisticated derivatives and secondary market trading strategies generating returns independent of market direction. They target 10-15% net returns.

Real estate funds acquire properties, make capital improvements, and sell at higher valuations. They target 8-12% net returns. Private credit funds provide loans to mid-market companies banks won’t finance, earning substantial interest. They target 8-12% net returns. Infrastructure funds invest in essential assets like toll roads, airports, or utilities, earning stable long-term cash flows. They target 6-8% net returns.

Each category has distinct characteristics affecting suitability for your situation. Private equity and venture capital require the longest lock-ups (7-10 years) and highest minimums (250,000 to 1,000,000 dollars minimum). Real estate requires moderate minimums (50,000 to 250,000 dollars) with moderate lock-ups (5-7 years). Infrastructure requires moderate minimums with longest lock-ups (10-15 years) but most stable returns. Private credit requires moderate minimums with shorter lock-ups (3-5 years).

Understanding these differences matters because they directly affect your overall portfolio construction and liquidity planning. You might intelligently allocate 10% to venture capital for growth potential, 15% to private equity for operational excellence, 8% to real estate for diversification and inflation hedging, and 7% to infrastructure for stability and steady returns. That 40% allocation to alternatives, combined with 60% in public stocks and bonds, gives comprehensive exposure across multiple return drivers and risk characteristics.

The Fee Question: Are They Worth What You Pay?

Investors consistently ask directly: Are alternative investment fund fees justified? This question deserves honest analysis. A 2% management fee plus 20% performance fee is substantially higher than mutual fund fees of 0.5-1% annually.

But the relevant question is not whether fees are high in absolute terms. The relevant question is whether the manager generates superior returns exceeding those fees. If an alternative investment fund charges 3.6% in total fees but consistently delivers 15% net returns to investors, the fees are absolutely justified and excellent value.

If another fund charges the same fees but only delivers 5% net returns to investors, the fees destroyed substantial investor value. This is why thorough due diligence on the manager’s historical track record is not optional or nice-to-have. It determines whether you make or lose money over decades.

Tax Implications and Diversification Strategy

Taxes matter significantly for AIF investment returns and long-term wealth building. Unlike mutual funds with standard annual tax reporting, alternatives have complex and varying tax structures. You might receive distributions taxed as ordinary income, capital gains, or return of capital. Carried interest – the performance fees the manager receives – might have different favorable tax treatment than your returns. Some alternatives might generate tax-inefficient ordinary income requiring annual tax payments on unrealized gains.

Other alternatives might defer capital gains until the exit event, providing beneficial tax deferral. Understanding the tax implications before committing capital matters substantially. Consult with a tax advisor familiar with what is an alternative investment fund tax treatment. The tax consequences can be significant relative to your net returns.

Getting Started: Practical Next Steps

If you have decided AIF investment makes sense for your situation, what are your specific next steps? First, ensure you meet accredited investor requirements: net worth exceeding 1,000,000 dollars excluding primary residence or income exceeding 200,000 dollars annually.

Second, honestly assess your capital situation. Do you have genuinely committed capital you can confidently lock away for 5-10 years?

Third, educate yourself extensively about different strategies. Read case studies. Understand fund structures. Learn how managers actually add value in practice.

Fourth, evaluate specific opportunities and funds. What strategies align with your personal investment goals? What are manager track records really showing?

Fifth, perform thorough due diligence. Review complete 10-year returns. Understand fee structures in detail. Request and contact investor references.

Sixth, start with modest commitments. Make your first what is an alternative investment fund investment a learning experience. 50,000 to 100,000 dollars is reasonable for your first commitment while you build real experience and develop conviction about manager quality. Do not commit your entire allocation to alternatives from a single manager. Diversify across multiple funds and multiple managers to reduce single-manager risk.

How Gamma Prime Helps Serious Investors

Accessing quality alternative investment funds has historically been difficult for investors outside elite financial networks and old money families. Opportunities are opaque. Managers only accept calls from institutional clients or ultra-wealthy families with established relationships. Minimum investments are prohibitively high for most investors. This is beginning to change due to technology. Gamma Prime connects serious accredited investors with world-class alternative investment funds across all categories.

We provide transparent information about fund strategies, manager track records, fee structures, and historical performance. We help you navigate complex due diligence. We handle administrative complexity. We help you understand what is an alternative investment fund so you make informed decisions aligned with your goals. Create your Gamma Prime account today to access alternative investment funds previously available only to ultra-wealthy individuals. Wealth is built where capital actually works. That is increasingly in alternative investment funds. It is time to participate.

Conclusion: Is This Right For You?

Understanding what is an alternative investment fund answers investor questions about returns, fees, liquidity, manager selection, and realistic expectations. Alternative investment funds offer genuine opportunities to enhance returns and diversification beyond traditional stocks and bonds. But they are not for everyone. They require sufficient capital, long time horizons, low liquidity needs, and willingness to evaluate managers carefully. If these conditions apply to you, meaningful allocations – 15-30% of your portfolio – to quality alternative investment funds can meaningfully improve lifetime wealth.

The answer to whether you should invest depends entirely on your personal situation, not on the funds themselves. Make this decision thoughtfully, with proper due diligence, and with conviction about manager quality. Your financial future may depend on getting this right.

In practice, successful participation in alternative investment funds comes down to discipline and clarity. Investors who approach this space with clear allocation strategies, defined risk tolerance, and realistic expectations tend to outperform those chasing short-term narratives or headline returns. It is essential to understand not only the upside potential but also the structural risks involved, including lock-up periods, capital calls, and varying liquidity profiles across different fund types.

Another key factor is manager selection. Unlike public markets, where performance is often driven by broad market movements, returns in alternative investments are highly dependent on the skill, experience, and strategy execution of individual managers. This makes due diligence not optional, but central. Reviewing past performance, understanding downside protection mechanisms, and evaluating alignment of incentives between managers and investors are all critical steps.

Gamma Prime simplifies this process by standardizing access to high-quality data and providing a structured environment for evaluation. Instead of relying on fragmented information or informal networks, investors gain a clear, comparable view of opportunities. This reduces informational asymmetry and allows for more rational, data-driven decision-making.

Ultimately, alternative investments are not about replacing traditional portfolios but enhancing them. When used correctly, they can provide uncorrelated returns, protect against market volatility, and open exposure to sectors otherwise inaccessible. For investors ready to take a more active role in managing their capital, this shift represents not just an opportunity, but a strategic advantage.

A practical approach is to start with a smaller allocation, build familiarity with different fund structures, and gradually increase exposure as confidence grows. Diversification across strategies – such as private credit, hedge funds, and real asset-backed opportunities – can further improve risk-adjusted returns while reducing dependence on any single manager or market cycle.

Consistency matters more than timing in this space. Investors who commit to a long-term framework and avoid reactive decisions tend to capture the full value of alternative investments. Over time, this disciplined approach compounds into a more resilient, better-balanced portfolio positioned to perform across varying economic environments.